So last July I suggested that the Fed was behind the curve and while Treasury yields were likely to go lower in the short term, ultimately coming into this year with tight labour markets inflation would be picking up and the Fed would look massively behind the curve and yields would have to reset higher.

That is more or less what happened, and even without the Ukraine war pushing up oil prices, wage inflation is driving service inflation and services are most of the US economy:

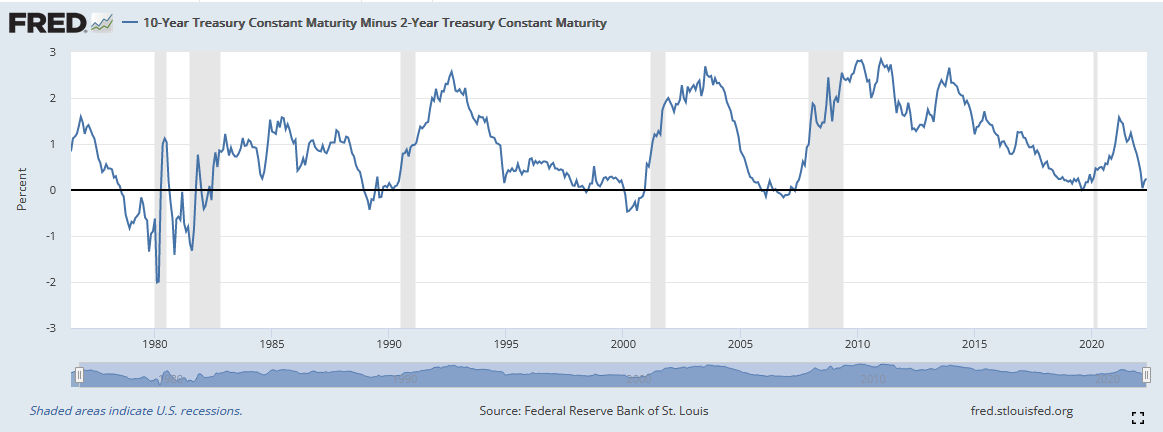

And with the Fed talking up 50bps a meeting until they get to a 'neutral' 2-2.5% Treasuries have repriced to about 3% on the 10 year, and a modest amount of curve steepness priced in for when the Fed finishes hiking.

So is this pricing accurate? Within the context of an ongoing recovery and inflation way above 2% target, the Fed has a legal mandate to bring it down via tightening, and that is what is priced and what they have been talking up recently.

However many leading indicators like sentiment and new orders are heading towards contraction or levels associated with a recession scare.

April saw quite a lot of sequential MoM slow downs (yellow highlight) in the CPI components, and outright energy price falls reduced the Core number from 0.6% MoM down to a headline CPI of 0.3% MoM. Some areas of ongoing sequential increase (blue highlight) should slow down as the Fed hikes.

Looking at the NY Fed UIG inflation measure,

CPI tends to be more volatile but mean reverts back (and through) the

UIG measure. That may imply headline CPI heads towards 2-3%, or lower,

in coming months as the volatile parts go flat or negative YoY.

So with everything that has happened (wages up, unit productivity down, costs like commodities up, margins squeezed, the Ukraine war related uncertainty, stimulus money gone and sentiment and new orders heading into contraction territory, China affected by Covid again etc) we are heading into a US growth slowdown.

That should take the heat out

of commodity prices and therefore both headline and core inflation.This

then opens the door for the Fed to come up with excuses and only go

25 bps at some meetings or even miss a meeting hike.

That should initially trigger equity and fixed income rallies. But as the slow down continues into the summer equities should fail to make a new high and then sell off again while US 10yr yields head towards maybe 2%. So the equity rally, fail, fall pattern could look something like below:

So assuming Fed back peddaling on rate hikes, cooling commodity prices and inflation pressures plus ongoing fiscal support cause the indicators to turn back up into year end, we could see at that time, say Q4 or going into Q1 or Q2 next year within the context of an ongoing US expansion yields rise closer to 4 or 4.5% on the 10yr Treasury.

And that may be enough for a genuine recession in late 2023.

Well, the Fed has proven what you know........

ReplyDeletethe US 10yr yield went to 2.51% at the end of July, roughly a 100bps reversal of the prior high in mid-June as the market looked for a growth scare that never really materialised in the hard data, only the soft survey data.

ReplyDeleteThe economy did then accelerate in Aug/ Sept and now the 10yr is nearly at 4% and looking to go towards 4.5% I think and equities have sold off. I think we can have a bear market equity rally now to the low 4000s and then a bigger sell off into year end.

I now think a US recession, ie job losses to speak of will likely be in Q1 next year not the second half of 2023.