My views are roughly as follows:

- Post-08 cycle led by US and China and credit spending/ rate cutting is basically finished, not quite finished but heading towards the end.

- If the Fed went to neutral interest rates, say 5%, we would have a recession

- However, Fed is loose and likely to stay loose (the Real Estate/ LBO Fed/ Whitehouse).

- We also have MAGA as a theme in the political economy and more generally the Fourth Turning drivers, or Global Trumpism as Mark Blythe calls it.

- So my idea is that with continuing low rates we enter a new economic cycle without a recession, we are seeing early signs of this last year with wages growing faster than GDP and manufacturing rebounding.

- In otherwords we have some sectors in recession, e.g. oil/ mining/ manufacturing, 2014-16, other growing and overall GDP slow positive growth. Next recession sectors: retail, retail real estate, consumer credit dependent businesses, companies dependent on cheap labour and cheap debt so quick service restaurants, weak companies with low margins (ie corporate zombies) etc

- Fed hikes a bit, to say 3%, defaults grind higher, overall GDP growth is a bit slow, wages grow as a % of GDP, corp profits decline as a % of GDP, govt tax base improves as wages rise, savings rate goes up, domestic manufacturing does well, CA deficit shrinks. oil production continues to rise. Basically it's Michael Hartnett’s Main Street > Wall Street theme.

- So new cycle drivers: wages rising as a % of GDP and then spent, oil production up, manufacturing and investment up. New industrial revolution: robotics, other new manufacturing processes such as combining image recognition with manufacturing, self-driving vehicles, automated warehouses, EV cars go mass market, other areas of nanotech going commercial, clean energy prices continuing to fall, energy storage being adopted, more medical technology breakthroughs leading to longer life expectancies and keeping baby boomers ‘alive but unwell’ for longer.

- Real assets with pricing power do well benefitting from the increase in revenues linked to GDP or these growth driver sectors.

- Companies lacking pricing power, too dependent on low wages, global supply chain, cheap credit, zombie companies etc do badly/ disappear. This killing off of the zombies will be positive for productivity and wages in aggregate.

- A good example is fast food. McDonald's can automate almost all of its food production. Whereas a salad bar, sandwich shop, or say an Italian food restaurant will really struggle to replace people with machines anytime soon.

- I think baby boomers spending as much money as they need to stay alive is also an interesting theme in medical technology, so they will be live but unwell and needing multiple treatments in their retirement

- I also think EM entered a new cycle in March 2016. EM real estate in some markets seems cheap to me, credit spreads and equity earning yields are low. Private credit is attractive. There is probably scope for interest rate cuts in some of the stressed markets such as Egypt and Turkey.

- Oil entered a bull market in March 2016 that will ($100 target +/-$10) peak as EV cars break through to mainstream

- EV cars just need a cheap battery technology breakthrough such as graphene supercapacitors. It seems this technology is almost ready to go into production.

- I think Greece is recovering

- Balkan EU accession process is interesting

- Puerto Rico post restructuring will be interesting

- Vene has a chance to change but probably won't and I cant see a catalyst for the bonds unless they somehow start paying them again.

- I think pension liability driven financial crisis will hurt Connecticut, Kentucky, Illinois and other states

- There are some interesting credit dispersion trades in US municipal bonds. Buying Puerto Rico post restructuring is one such trade

So what could block this and cause a 2018/2019 recession? A rapid rise in the savings rate, rapid liquidation of inventories as a response to margin squeeze, rapid Fed hiking.

I think is Fed keeps rates low and hikes slowly to a terminal rate that is loose for the real economy interest rate (say 3% Fed funds vs 5.5-6.5% nominal GDP growth), that is stimulative for the real economy but negative for the financial economy, but not negative enough to cause a financial crisis.

I think its more like the 1970s where financial assets go sideways for years while inflation and wages go up

However we are not quite there yet, financial assets are still doing OK, wages are a bit slow, and the Fed is still loose

Some people think Puerto Rico could become like a Singapore. Most US states will have to increase taxes to cover pension and healthcare costs for baby boomers who started retiring in the last 2 years. The weakest states are already nearly bankrupt. But if you relocate to Puerto Rico then you pay something like 4% corporation tax and no state income tax.

What if for most pensions the following assumptions are wrong:

- Returns go to near zero for a decade instead of making 7%

- Baby boomers spending on healthcare and medical breakthroughs keep people alive for an extra few years, but at great cost

- Nominal GDP starts rising 6 or 7% a year (currently 5.5%)

- Min wages rise, a lot of government jobs are basic paying, a lot of healthcare jobs are too.

- If they increase their required yield to 8 or 9% as a result of all of this, then all the numbers for unfunded pension liabilities are going in the wrong direction.

We just had a 35 year asset market super cycle and the pensions are still underfunded....

US states can not default on debt. Some can restructure contractual liabilities such as pensions, eitherway taxes are likely to go up at the state level in many states.

Cities and municipalities can default. So you can get a pension fund 'run on the bank' where people start to cash out their pensions before the city or municipality defaults

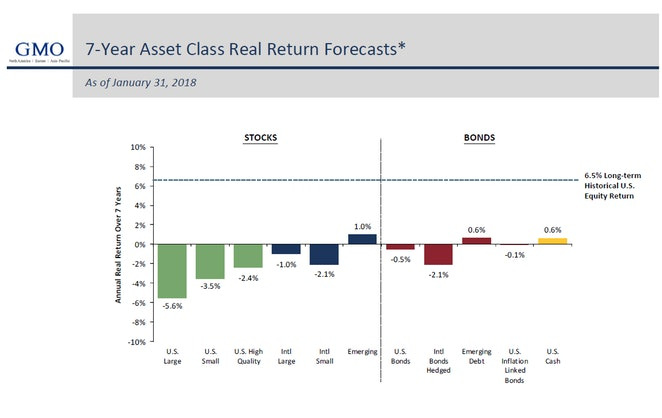

GMO forecasting negative returns for balanced portfolios.

Source: GMO

No comments:

Post a Comment